Comparison of Major Supermarkets in Australia — Part 2 (Product Category Segmentation, Specials, and Private Labels)

For details on the data analysis (view notebook file here)

Total Number of Unique Products Stocked

- IGA — 1787

- Coles — 20,826

- Woolworths — 22,338

Product Category Segmentation

IGA, Woolworths and Coles separates their products into the following categories:

IGA and Woolworths seems to have an almost identical product category naming convention. Coles also has numerous similarly named categories, except it has a few additional categories which may usually be considered as belonging to subcategories. In order to conduct any meaningful analysis, the category names across all three supermarkets need to be standardized.

The following transformations were made to the Category column of each supermarket:

IGA:

- ‘And’ is replaced with ‘&’.

- ‘Meat’ is replaced with ‘Meat Seafood & Deli’.

Woolworths

- ‘Freezer’ is replaced with ‘Frozen’.

Coles

- Removed ‘Kids’ from ‘Kids Lunch Box’, so it now becomes just ‘Lunch Box’.

- ‘Dairy Eggs Meals’ replaced with ‘Dairy Eggs & Fridge’.

- ‘Fruit Vegetables’ replaced with ‘Fruit & Veg’.

- ‘Meat Seafood Deli’ becomes ‘Meat Seafood & Deli’.

- ‘Health Beauty’ becomes ‘Health & Beauty’.

The bar charts above provide us with some insights into the percentage of total products allocated to various categories. However, there are quite a few unmatched ‘odd’ categories i.e. ‘International Foods’, ‘Entertaining At Home’, ‘Mothers Day’, ‘From Deli’, and ‘Convenience Meals’ from Coles, and ‘Grocery Packs’ and ‘Other ’from IGA.

A quick look over the datasets in MS Excel reveals that most of the products in the ‘odd’ categories are duplicated in other ‘core’ categories. It would make the comparison much clearer if duplicates in these ‘odd’ categories were removed. The remaining items can be manually looked over, and a judgement made, to re-allocate them to the appropriate (core) categories — which are common to all three supermarkets. This will effectively standardize the ‘core’ categories across all three supermarkets, making the product category segmentation analysis much clearer and informative.

Removing Duplicated Items and Re-categorizing remaining items from the ‘odd’ Categories

Coles

- The following duplicated items have had their entries removed from the following categories:

‘Entertaining At Home’, ‘Mothers Day’, ‘International Foods’, ‘Lunch Box’, ‘From Deli’, ‘Convenience Meals’. - The remaining list is outputted into a CSV file and examined with MS Excel — to be manually examined and a judgement made on how best to re-allocate the remaining items.

Looking through the CSV file, almost all of the 975 items in the list can be classified as ‘Pantry’ items — searching for some of the same products on the Woolworths websites confirms this assertion. There are 40 items which have ‘Drink’ or ‘Juice’ in their product name. They are re-allocated to the ‘Drinks’ category.

The remaining items:

- Anything labelled ‘From Deli’ is moved to ‘Meat Seafood & Deli’.

- ‘Convenience Meals’ moved to ‘Frozen’.

- ‘Lunch Box’ items moved to ‘Pantry’ — with the exception of the following items which were moved to ‘Household’:

[‘Riverside Drink Bottle 517mL’, ‘Stainless Steel Bottle Special’, ‘Bento Bite 6 Compartment Box’, ‘Back Pack Boys’, ‘Leak Proof Snack Box’, ‘Consumption Bottle 1L’, ‘Leak Proof Sandwich Box’, ‘Back Pack Girls'] - ‘Entertaining At Home’ items moved to ‘Household’ — with the exception of the following items which were moved to ‘Meat Seafood & Deli’:

[‘Smokey Bacon & Cheese Sausages’, ‘Beef Eater BBQ Sausages’, ‘Beef Bacon & Cheddar Sausages Bag’, ‘Lincolnshire Sausage Bag’, ‘Pork Cumberland Sausage Bag’, ‘Thin Pork Sausages Bag’]

Woolworths

- Removed duplicated items from ‘Lunch Box’.

- [‘V8 Tropical Juice’, ‘Woolworths Spring Water Minis’, ‘Appy Co Tropical Fruit Drink’, ‘Appy Co Summer Berries Fruit Drink’] — moved to ‘Drinks’.

- [‘Celery And Philly Afternoon Snack Solution Bundle’, ‘Woolworths Celery Sticks’] — moved to ‘Fruit & Veg’.

- All remaining items moved to ‘Pantry’.

IGA

- Removed ‘Other’ and ‘Grocery Packs’ — these are just bundles of individual items listed in other categories.

The modified DataFrames from above outputted as CSV files here.

In the next post, these files will be used for fuzzy matching to find and match identical products for direct product-to-product comparisons.

After the above modifications (removal of duplicates and consolidation of categories), we can now see a much clearer picture of the comparison between Woolworths, Coles and IGA in relation of their product category segmentations.

Insights:

- Generally, there isn’t a large difference in most of the categories between Woolworths and Coles in terms of the number of products stocked. In terms of percentage of total items stocked, it’s also very similar. The exception is in Household, where Woolworths seems to have significantly more products, both in raw numbers and as a percentage of total items. So, if you’re looking for kitchen or bathroom paraphernalia, then Woolworths should have the highest likelihood of having what you’re looking for.

- IGA predominantly focuses on Pantry (almost 50%), Drinks, Household and Health & Beauty — all of which have a very long shelf-life.

- IGA stocks less perishable products such as ‘Dairy, Eggs & Fridge’ and ‘Meat Seafood & Deli’, but surprisingly have a relatively larger ‘Fruit & Veg’ selection.

- The category names used by each supermarket suggests that IGA focuses on/uses Woolworths as some sort of pricing/product offering benchmark — this is further confirmed by comparing individual product names between Woolworths and IGA. Coles have listed some unusual additional categories, which some may consider as subcategories, in their main categories e.g. ‘International Foods’, ‘Entertaining At Home’, and ‘Convenience Meals’.

Products ‘On Special’ as % of Total Products

- Coles has a larger percentage of products on special than Woolworths.

- For both supermarkets, the greater majority of products on special are in the Pantry, Health & Beauty, Household and Drinks categories.

- Coles has significantly more of their Pantry products on special than Woolworths.

- Woolworths has significantly more of their Health & Beauty products on special than Coles.

- This is only a cross-sectional observation — a time series look of these comparisons may reveal that (potentially) these differences flip over time i.e. when Coles discounts more of their Pantry, Woolworths focuses their discounts on Health & Beauty and vice versa depending on which cycle of discounting they’re going through.

The Impetus for Own-Brand Private Labels

To understand why there has been a recent shift from both Woolworths and Coles towards having their own private labels, we must look at the impact Aldi’s entrance has had on the industry.

As the saying goes, a picture is worth a thousand words. It is very clear from the above charts depicting changes in market share that Aldi has been ‘eating [the incumbent’s] lunch’ in the past decade.

TLDR: Coles is focusing on profitability by increasing own-brand private labels, and Woolworths has adopted a cost leadership strategy to maintain and increase market share by sacrificing margins. Woolworths have also created an internal NSA-like ‘data analytics’ and ‘consumer insights’ division.

According to IBISWorld’s Supermarkets and Grocery Stores in Australia Industry report:

“Consumer sentiment is anticipated to fall and become negative, and unemployment is expected to increase sharply in 2019–20. Many consumers are anticipated to increasingly opt for cheaper goods, such as private-label brands, as poor consumer sentiment constrains expenditure.”

“Industry profitability is projected to increase over the next five years. An anticipated decline in price-based competition, in conjunction with efficiency-boosting strategies from major players, will likely aid margin growth. While private-label goods typically have lower prices than branded alternatives, own-brand products are more profitable for supermarkets. The continued shift towards private-label brands is forecast to support industry margins over the next five years.”

“Over the past five years, Coles has been increasing the proportion of its own private-label goods. Coles has indicated it will continue to grow its private-label product range, implementing a strategy undertaken by many supermarkets in international markets. Coles intends to increase the share of total sales generated from its private-label products from 20% to 40% over the next five years. Sales of private-label goods are typically more profitable for supermarkets than sales of branded products. This factor makes the shift towards more own-brand products attractive for industry operators, including Coles. While the company has attempted to increase its market share over the past decade, Coles is forecast to shift its focus to boosting profit margins over the next five years.”

“Woolworths has had more success in online grocery sales than major competitor Coles. Woolworths invested heavily in building click-and-collect infrastructure in stores, which has been successful with consumers. However, the company’s strategy of lowering prices has reduced its industry-specific profitability over the past five years. While Woolworths’ margins have fallen over the period, this masks the strong rise in margins over the past three years. Profit has recently risen due to increased store traffic, as consumers have increasingly approved of Woolworths’ pricing and improved in-store experience.”

“Woolworths introduced WooliesX, an internal agency dedicated to digital, data and customer insights, in July 2017. The company has also invested more in consumer data analytics, purchasing a 50.0% share in data analytics company Quantium. In October 2018, Woolworths awarded Quantium a contract for sales data sharing and research services.”

It is worth noting that Woolworths removed access to their public API in the past year but have promised that it will be back. They have also incorporated very sophisticated anti-scraping defenses. With Aldi’s ecommerce platform close to being fully operational and the imminent threat from Amazon entering the Australian online groceries market, Woolworths may be pre-emptively defending their cost leadership position by proactively putting up barriers against price intelligence collection — as evidenced by this public notice on the Price Hipster website. Coles, which had a public API many years ago, has been notorious for being a difficult website to scrape for many years, most likely due to their inability or unwillingness to compete with Woolworths on price… a hypothesis which will be tested in part 4.

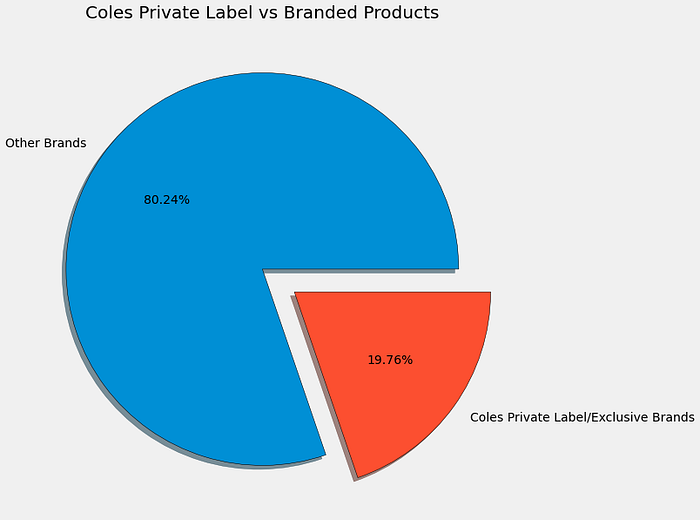

Private Labels as a % of Total Products

List of Coles Private Label and their Exclusive Brands:

- Coles (and any Brand with Coles in it e.g. Coles Finest, Coles Organic)

- Cook & Dine

- Wellness Road

- I’m Free From

- Nature’s Kitchen

- Wild Tides

- Daley Street

- I’m Perfect

- Slow Hills

- KOi

- Woofin’ Good

- Green Choice

- GRAZE beef and lamb

- CUB

Sources:

- https://www.coles.com.au/about-coles/exclusive-brands

- https://www.colesgroup.com.au/media-releases/?page=quality-kitchenware-sizzles-at-coles

List of Woolworths private labels and exclusive brands:

- Woolworths (and any label including Woolworths in their name)

- Sam’s Pantry

- Thomas Dux Range

- Farmer’s Own Milk

- Macro

- Essentials

- Bunch

- Frey

- Little One’s

- Voeu

- Apollo

- Baxters

- Your Majesty

- Smitten

- La Molisana

Source: https://www.woolworths.com.au/shop/discover/our-brands

The pie charts above shows that the proportion of private labels as a percentage of total products at Coles is almost double of Woolworths.

Private Labels in each Category

From the above bar charts we see that Coles stocks more private label products in every category than Woolworths. In percentage terms, almost all of the Fruit & Veg products at Coles are now own-branded (i.e. Coles brand). More than 50% of the products in Bakery, and Meat Seafood & Deli are private labels at Coles.

It would be interesting to track any changes in the percentage of private labels of both Coles and Woolworths, in a monthly or quarterly period, over the next 5 years. It may provide an early indication of a pivot in strategy.

Insights:

- Aldi’s success in capturing market share in the last decade has prompted a pivot towards private labels — especially at Coles.

- Coles has a larger proportion of their products on special than Woolworths — almost twice as many.

- Coles, in percentage of total products terms, has almost twice the amount of private labels as Woolworths.

- In every single category, Coles has more private labels, as a percentage of the total items in the category, than Woolworths.